A more positive production outlook is expected across the shrimp and fin-fish aquaculture sectors next year, according to the findings of the latest seafood industry survey conducted by Rabobank and the Global Seafood Alliance (GSA).

Summarised in Rabobank’s new “What to Expect in the Aquaculture Industry in 2024” report, the survey’s respondents expect global shrimp production to recover in 2024, albeit at a lower rate than the 10-year historical average. The survey results forecast a year-on-year shrimp production growth of 4.8% in 2024, surpassing 2022’s peak volumes, after an expected modest decline of 0.4% in 2023.

In Ecuador – the world’s leading shrimp producer – the production growth is expected to decelerate in 2024.

“While continued growth is anticipated, milder expectations may be a result of El Niño-related uncertainty, as potential strong El Niño conditions pose downside risks due to heavy rains, which can increase flooding risks and potentially damage the infrastructure of ponds in Ecuador,” Rabobank Seafood Analyst Novel Sharma said.

There is optimism for Asian shrimp production, with survey respondents forecasting a potential recovery of 4% in 2024, following the region’s first decline in a decade in 2023.

“This will depend on prices improving in 2024 after the continuous downward trend in 2023, which made the majority of the industry unprofitable,” Sharma said.

Likewise, production in India and Vietnam are set to recover in 2024, following sharp contractions in 2023. Whether both regions achieve their forecast production growth in 2024 will depend on demand improvement in the US and Europe and prices recovering sufficiently to incentivise farmers to increase stocking of ponds.

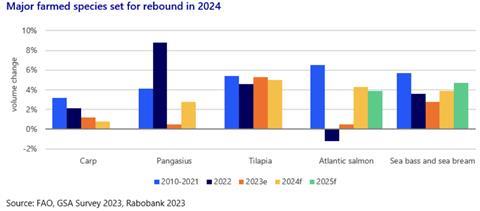

In the fish farming sector, the major farmed species of salmon, tilapia, pangasius, seabream and seabass are all expected to grow in volume terms, although El Niño poses potential downside risks for some species and regions, offers the report.

It advises that after two consecutive years of weak global production growth, global Atlantic salmon production reached an inflection point in the third-quarter of 2023, and provided there are no unforeseen biological issues or events, global production is expected to grow by 4.3% and 3.9%, respectively, in 2024 and 2025, led by Norway.

However, uncertainties remain around Chile’s potential volume growth over the next few years due to new legislation and biological issues, and it is unlikely that production volumes will eclipse 2020 levels before 2025. Additionally, there are potential downside risks heading into 2024, as higher temperatures due to El Niño conditions may lead to higher incidences of algal blooms, causing an increase in mortalities.

But Rabobank also notes the industry is better equipped to deal with potential downsides now than it was during the last El Niño event.

After a pause in 2020, global tilapia production began gradually recovering and is expected to grow by 5.3% year-on-year in 2023 – eclipsing 2019 volumes. Strong growth is anticipated in Asia, particularly in Indonesia, though China is expected to maintain its position as the top tilapia producer in the near-term.

However, if consumers continue to favour premium species, China’s fish farmers could change the species they produce, potentially decelerating tilapia production growth, suggests the report.

Last but not least, the survey also asked industry experts about their concerns for the coming year. Market prices topped the list, as uncertainties remain about the effects of persistent inflation and the recovery of seafood demand, while elevated costs and stagnating household disposable incomes remain challenges for consumers across major markets.

Consumers may look to trade down, either within the seafood category or to lower-priced protein options, Rabobank said.