Seafood demand is expected to decrease in the second half of 2022 compared with the past 12 months, according to Dutch finance company, Rabobank.

Softening demand, price corrections and high production costs will all affect salmon and shrimp farmers whilst fish meal prices are likely to be supported by the high price of alternatives.

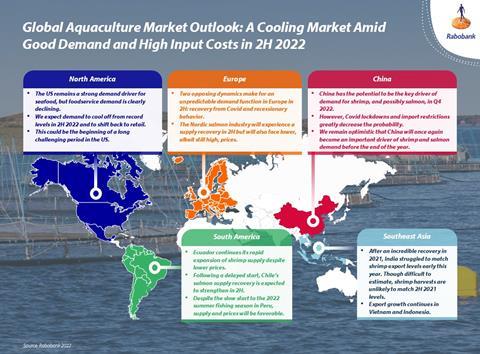

Rabobank’s latest report on aquaculture points to reducing demand for seafood in both the EU and US as countries struggle to recover from the economic effects of the pandemic. The situation in China is less certain and there is potential for increases in both shrimp and salmon demand provided lockdowns are not reintroduced.

“The US remains a strong demand driver for seafood, but foodservice demand is clearly declining,” said Gorjan Nikolik, senior global specialist, seafood at Rabobank. “But China has the potential to be the key driver of demand for shrimp, and possibly salmon, in Q4 2022.”

Costs to remain high

Feed, freight and energy costs are expected to remain high or even increase in the second half of the year. For salmon farmers, a large part of 2021 and early 2022 was marked by record profitability, driven entirely by high price levels. However, due to the long production cycle, high feed costs have yet to be fully felt although profitability is still expected to remain healthy.

In contrast, if shrimp supply continues to expand farmers may struggle to break even. “We remain optimistic about the long-term prospects of the shrimp industry but expect a challenging period in the short term,” said Nikolik.

Meanwhile, fish meal supply remains relatively stable. However, the record prices of vegetable substitutes make marine ingredients relatively competitive in feed formulas, supporting demand and prices.